日経平均株価↓ -14.90% -3055円 終値17450円 (前日終値20500円)

これは1987年10月19日(月)の「ブラック・マンデー」から一夜明けた翌日20日(火)の日経平均株価の下落率「-14.90%」を、現在のマーケット水準(日経平均20500円)に合わせた架空のニュースです。もちろん現在は当時とは値幅制限の制度が違いますので、現実には違った運びとなるでしょう。

ブラック・マンデーは全てのトレーダーにとって最も重要な教訓の一つです。当時の株価や為替の動向が記録された書物は多く存在します。しかし「あの日のオプション市場」について書かれた物はほとんど見掛けることはできません。少ない情報ですが、当時の「S&P500オプション」について今回のレポートでまとめてみます。

ブラック・マンデーのような極端な錯乱的状況下に於いて、わたしたちはマーケットで適切な対応ができるのでしょうか。今、ご自分が抱えているオプション・ポジションと照らし合わせて、追体験をしてみましょう。

まずブラック・マンデーの概要です。

ブラック・マンデー(暗黒の月曜日)

1987年10月19日(月)に史上最大の株価大暴落が起きた。この大暴落は現在に至っても多くの投資家のトラウマとなっている。またこれ以前から繰り返されてきたバブル発生とその崩壊を学ぶ、最大の教訓ともなっている。

1982年8月に776ドルであったダウ平均株価は、1987年8月には2,722ドルまで上昇していた。このバブル成長期の取引高は3倍に膨れ上がり、世界の株価を平均296%押し上げた。

市場には楽観主義が蔓延しており、「株を買って・値上がりするのを待つ」、「株を買うだけで一儲けできる」、という話に乗らない者はいなかった。このときにも過去のバブル成長期同様に、「借金をしてでも株を持て」、「株を持たないやつはバカ」、と言われていたようで、大衆によって狂気が狂気ではなくなっていた。

まるで永遠に株価上昇を続けるかのような大衆の言動や、世間の楽観主義、そして天井を付けた後の高値波乱、これらの動向を注視している投資家は、大暴落の予兆に気が付いていたはずである。そして高値波乱のうちに売り抜けることができたはずである。これから未来にも同様のバブルがやってくるであろうが、そのときは決して大衆に飲み込まれてはならない、という教訓が得られる。

株価の崩壊は予兆もなく、また一夜にして起きたわけではない。前述のように株価の天井は8月に付けており、暴落は2ヶ月間の高値波乱の後に起きた。

実際の株価の暴落は、ブラック・マンデーの前週10月14日から始まっていた。ブラック・マンデーとは、この一連の暴落が最大幅となった「セリングクライマックス」の日のことを指す。

10月14日(水)

・ダウ平均株価指数 ↓-3.81%

10月16日(金)

・ダウ平均株価指数 ↓-4.60%

10月19日(月)〔ブラック・マンデー〕

・ダウ平均株価指数 ↓-22.6% (史上最大の下落率)

・S&P500種指数 ↓-20.4% (最大↓-30%)

10月20日(火)

・日経平均株価↓-14.90% -3,836.48円 終値21,910.08円

この日の日経平均株価は下落幅・下落率ともに過去最大のものとなった。東証1部銘柄の半数がストップ安した。しかし地球が半周周り、NY市場がオープンすると株価は世紀の大反転を果たし、史上最大の上昇幅となった。

ダイナミック・ポートフォリオ・インシュアランス

1985年に「ダイナミック・ポートフォリオ・インシュアランス」という、オプションを活用した新戦略が発表されました。これはカリフォルニアのLOR社(レーランド・オブライエン&ルビンシュタイン社)が開発したストラテジーで、現物株式ポートフォリオの値下がりリスクを、指数先物とプット・オプションを利用して完全にインシュアランス(保険)するストラテジーです。

ダイナミック・ポートフォリオ・インシュアランス戦略では、理論的に「現物株式のポートフォリオの損益+指数先物の損益 = プット・オプションの損益」、となります。

この運用方法では、運用担当者は現物株式のポートフォリオを調整する必要がなく、オプション価格式により算出された数量の指数先物の売り買いを継続的に行っていきます。現物株式のポートフォリオに手を付けずに済み、調整は指数先物の売買のみと非常に管理が単純であることから、このストラテジーは当時の機関投資家を中心に爆発的に普及しました。

リンカーン年金信託の運用担当役員ジョン・ストロングも、1986年の年初からS&P500の現物株式ポートフォリオに対して「ダイナミック・ポートフォリオ・インシュアランス」による運用を実行しました。そして1987年10月16日(金)までのおよそ22か月間はLOR社の宣伝文句通り、「非常にうまく機能していた」と言います。

ところが10月19日(月)から10月22日(木)までの4日間、「ダイナミック・ポートフォリオ・インシュアランス」は機能不全状態に陥り、リンカーン年金信託は巨額の損失を出しました。

S&P500の現物株式ポートフォリオの値下がりリスクを「完全に」インシュアランス(保険)していた運用ストラテジーのはずが、なぜ巨額損失を出すことになってしまったのでしょうか。

ボラティリティの暴騰により各市場が分断

それはブラック・マンデーという錯乱的マーケット環境に於いて、マザーマーケットである現物株式市場に売りが殺到し、ボラティリティが爆発的に上昇したことに起因します。その結果、普段では裁定により相関が効いていた現物株式市場と先物市場、そしてオプション市場が分断されました。

莫大な取引注文が入った現物株式市場のプライスが麻痺状態であるために、誰も先物価格の適正値を出すことができず、更にオプション市場も理論値を算出することができません。

よって現物と先物とオプションを組み合わせた運用方法である「ダイナミック・ポートフォリオ・インシュアランス」は、下落ヘッジのための適正な先物調整値の算出をすることが不可能となり、完全に機能を失いました。

ブラック・マンデーの週の最後の取引日、10月23日(金)にようやくボラティリティが落ち着きを取り戻すと、各市場間の相関も正常に戻り、「ダイナミック・ポートフォリオ・インシュアランス」も機能を取り戻しました。しかしそれはその週これまでの4日間で巨額の損失を出した後のことでした。

コール裸買い

またS&P500オプションの単純コール買い(コール裸買い)ポジションを取っていたという別の記録では、この爆発的なボラティリティの上昇がオプション価格に与える影響を生々しく伝えています。

ブラック・マンデーの前の週にS&P500のATM(アット・ザ・マネー)のコール・オプションを買い建て、その時のオプション価格は12ドル、IV(インプライド・ボラティリティ)は少し高めのおよそ20%だったといいます。そして週明け月曜日にマーケットをブラック・マンデーが襲い、S&P500は20%下落しました。

もちろん単独のコール・オプションの買いは、原資産価格の下落に対し、全く恩恵を受けないポジションであり、もしIVが20%のまま変化していないとすると、S&P500の20%下落により12ドルのコール・オプションはわずか3セントの価値しか残っていない計算になります。

しかし実際にはこのコール・オプションは、8ドル50セントで取引されていたといいます。これはIVが60%まで上昇していたことを示しており、20%もの原資産市場の下落によるコール・オプションの減価を、ボラティリティの高騰により相殺していたことになります。

このケースを円貨で例えると、3円となっているはずのコール・オプションが850円で取引されているのと同義ですから、ボラティリティの高騰はその特性によりオプション価格に破壊的な影響を与えるのです。

「ボラティリティがオプション価格に与える影響」に関するレポートはこちらをどうぞ。

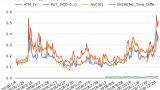

ATM60%の世界

ATMのIVが60%のとき、プットのOTM(アウト・オブ・ザ・マネー)やFOTM(ファー・アウト・オブ・ザ・マネー)のIVは、一体どのくらいの値となるのでしょうか。日経225オプションIVデータでイメージをしてみてください。

ブラック・スワンはいつか必ず姿を現す

9.11のとき前日7円で終わっていたプット・オプションは、翌朝705円で寄り付きました。昨今Weeklyオプションで流行っているように、残存わずか3日でしたのでプット裸売りをSQ持込みしようと考えていた人も多くいたことでしょう。ドストライクの「即死ポジション」です。そもそもマーケットが開ていないのですから、対応のしようがありません。

また3.11東日本大震災の翌週、マーケットの混乱とは別のところで問題が起きました。原発が吹き飛びマーケットが最も悲惨な状況下で、証券各社は緊急的にオプション売り建玉上限枚数を「ゼロ枚」まで引き下げました。証拠金に余裕があろうが、実質的な全オプション売建玉の強制決済です(カブドットコム証券とSBI証券はこの措置を取りませんでした)。

買玉と売玉と組み合わせた至極まっとうなスプレッド戦略ですら、大引けまでに解体せざるを得なくなりました。損失を抱えながらもボラティリティ低下や時間経過などオプション特性により、いずれ挽回できるであろうポジションを歯を食いしばりながら泣く泣く返した人もいることでしょう。

こちらで「3.11東日本大震災の一週間」をレポートしていますので合わせてどうぞ。

そして週明け月曜日を襲ったブラック・マンデー。原資産20%下落、ボラティリティの暴騰、そして現物・先物・オプション市場間の分断。続く翌日、翌々日の史上最大の上げ幅となる大反転。

天災、事件、事故、謎の暴落、マーケットにいれば突然やってくるクラッシュにいつか必ず巻き込まれます。

真のクラッシュに突然襲われたとき、不運にもそのとき抱えているポジションが不利となる場合、致命傷を負わずに乗り切ることができると言えるでしょうか。乗り切れるか否かで、その後の人生は180度変わります。オプション取引の最大の問題は、「ブラックスワン」と如何に付き合っていくか、ということなのです。

ブラック・スワン(上/下)-不確実性とリスクの本質(ナシーム・ニコラス・タレブ)はこちらで紹介しています。信者になる必要はありませんが、必読です。